Many are aware of the importance of investing one’s money but where do one start? Fret not, FLY Malaysia has one covered with their annual flagship event – Malaysian Youth Finance Series(MYFS) 2020. This event has many esteemed speakers such as William Chow, a Board of Director Affairs & Corporate Culture of China Construction Bank (Malaysia) Berhad, Steven Wong Weng Leong, Chief Operating & Financial Strategist (COO) China Construction Bank (Malaysia) Berhad, Ian Wong, Partner of IPP Financial Planning Group Malaysia, Kimberly Law, a senior associate of IPP Financial Planning Group Malaysia and many more.

Event Agenda

The event is split into 2 different sessions, each consists of a panel session and interactive activity. The 2 sessions focused on Investment and Personal Finance. The panel session will be covering the above topics to equip participants with necessary knowledge. The workshop will require participants to apply the knowledge learned via a case study or a discussion/ presentation.

Session 1: Investment

Best investment for a beginner?

Factors to consider when choosing an investment:

- Risk appetite

- Size of the investment (fund)

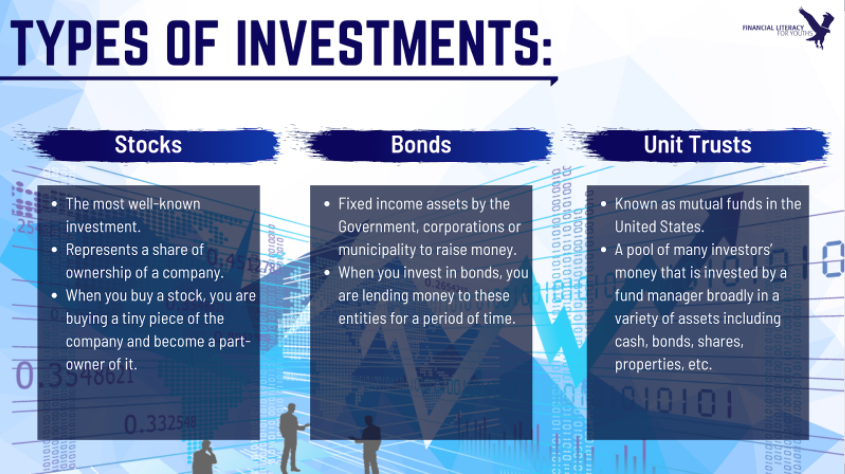

Types of investment:

- Stocks

- Bonds

- Unit Trust

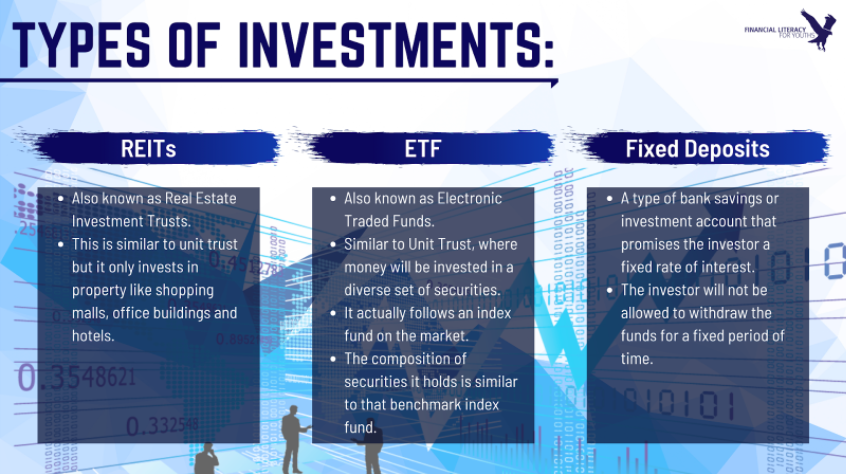

- Real Estate Investment Trust (REITs)

- Electronic Traded Funds (ETF)

- Fixed Deposits

Tips:

- One can opt for the direct stock if one has over a hundred thousand dollars/ringgit(?) of funds.

- Or Exchange-traded fund (ETF) if one wants to start small

The benefit of starting at a young age

- More room for growth

- Know the key concept of investment and how to maximise one’s investment

Financial freedom

- The key to achieve financial independence is investing

- Identify the specific financial freedom that one wants to achieve

- Make sure one has interest

- Do not follow the fund managers who are against your interest.

Q&A Session

Q1: What is your view on micro-investing platforms such as Raiz and StashAway? Is it a good start for students? Thank you.

Ian Wong: The tools are good, but you have to identify your personal interest.

StashAway may not be the best for people who like to watch the market. It is more for less aggressive investors who do not have the time to monitor the stock.

Q2: What’s your opinion/take on students beginning to invest by starting with fixed deposits? Is it advisable to distribute the fixed deposit units to other sources of investments or should we stay safe by relying on the fixed deposit instead?

Ian Wong: Fixed deposit interests are low globally now. Hence it is not advisable to invest solely in fixed deposits.

Q3: I’m interested to know more about how we can evaluate how the fund manager/the company that manages the fund, i.e. in the unit trust or shares when making investment decisions. I would appreciate it if you can recommend any useful resources or methods to perform this kind of evaluation. Thank you!

Dr. Kim Hwa Lim: Usually, fund managers will invest in growth companies which have a lot of room to increase their revenue. Choose the fund manager which suits your investment preference.

Session 2: Personal Finance

The following session is conducted by Kimberly Law. In order to simplify the process, personal finance can be differentiated into 4 categories:

- Cashflow management

- Asset allocation

- Risk management

- Debt management

“Personal finance is like a car, one needs petrol to move (cashflow), engine to start (growth investments), brakes for safety (secure investments) and handbrake, just in case the brakes didn’t work (insurances).” said Ms Kimberly. Personal finance is a lifelong journey where one needs to set their destination. In this case, setting up short-term goals while making one’s way to one’s long-term goal which is financial freedom.

A general rule of thumb to achieve financial freedom with the following formula:

Financial Freedom = Desired House + 10 times of current annual income

Let’s say Alex has an annual income of RM100,000 and 10*100k = RM1mil. Thus,

- Annual savings = RM10k (10% of annual income) → 100 years to reach RM1mil

- Annual savings = RM20k (20% of annual income) → 50 years to reach RM1mil

- Annual savings = RM30k (30% of annual income) → 33 years to reach RM1mil

- Annual savings = RM40k (20% of annual income) → 25 years to reach RM1mil

- Annual savings = RM50k (50% of annual income) → 20 years to reach RM1mil

Cashflow Management

Income – savings = expenses

Ms Kimberly stated that ideally, net income is to be distributed into savings, living expenses and fun funds. Savings can be categorized into future investments and emergency funds; Living expenses are one’s fixed expenses such as monthly repayment of loans, subscriptions and variable expenses such as credit card, e-wallet, etc; Last but not least, the fun fund being travel expenses and desired goods.

Asset Allocation

At 20’s, focus on generating as much capital as possible by making the right investment.

At 40’s, shift that focus to passive income.

Asset Portfolio

Having a strong foundation is important to build a sustainable portfolio. Therefore, one should start investing in less risky assets such as EPF, bond endowments, etc. Eventually, move their way up as the risk level increases by investing in stocks, unit trusts, ETFs, REITs, etc.

If property investing is what tickles one’s fancy, there are few rules that might help one’s journey. One should be aware of the difference between buying a home or investing in it. With that being said, one should take their time in choosing the right one and don’t rush.

Rules for home:

- One likes the place

- Affordability

Rules for property investment:

- Initial costs

- Maintenance & operating costs

- Potential customers

Risk Management

A common misconception of insurance is that people tend to associate it as an investment. Thus, they believe that the more they buy, the better it is for them. However, insurance is a risk management tool, a cost incurred monthly which can be excessive for some to repay. Insurance can be classified into 3 types:

- The ones that pay policyholders

- The ones that pay policyholder’s family

- The ones that pay the hospital

Debt Management

Most Malaysians are affected by all kinds of loans such as car loans (59%), mortgage (50%), personal loan (49%), credit card (39%), student loan (23%) and non-bank loans(?)(15%). A good loan can come a long way while a bad loan can haunt a person for the rest of their life. Thus, before taking up a loan, consider these few factors:

- Does one really need it?

- Does it improve oneself?

- Does it increase one’s current income?

What’s a good and bad loan? Outcomes may vary to circumstances

- Good Loan

- Student loan

- Business loan

- Mortgage

- Bad Loan

- Personal loan

- Credit card

- Car loan*(could be a good loan if it helps one to get more client/ improve business)

Tips to decide on one’s loans:

- Familiar with the terms and conditions

- Consider one’s monthly cashflow, payment period, interest rates

- Possible fees involved

- Possible early settlement discount/ rebate

Myths on loans:

- Settle loan faster (overpaying monthly, unless there is a discount)

- Take shorter loan to save on interest (affects cashflow)

- Refinance / consolidate debts

- To be more creditworthy

- Agensi Kaunseling & Perundingan Kredit (AKPK) is bad

Myths on credit card:

- Bad to have credit card

- Buy things that exceed one’s affordability

- Pay minimum every month

How to detect a scam? It is only possible to have 2 of the 3 characteristics!

- Liquidity

- Return

- Safety

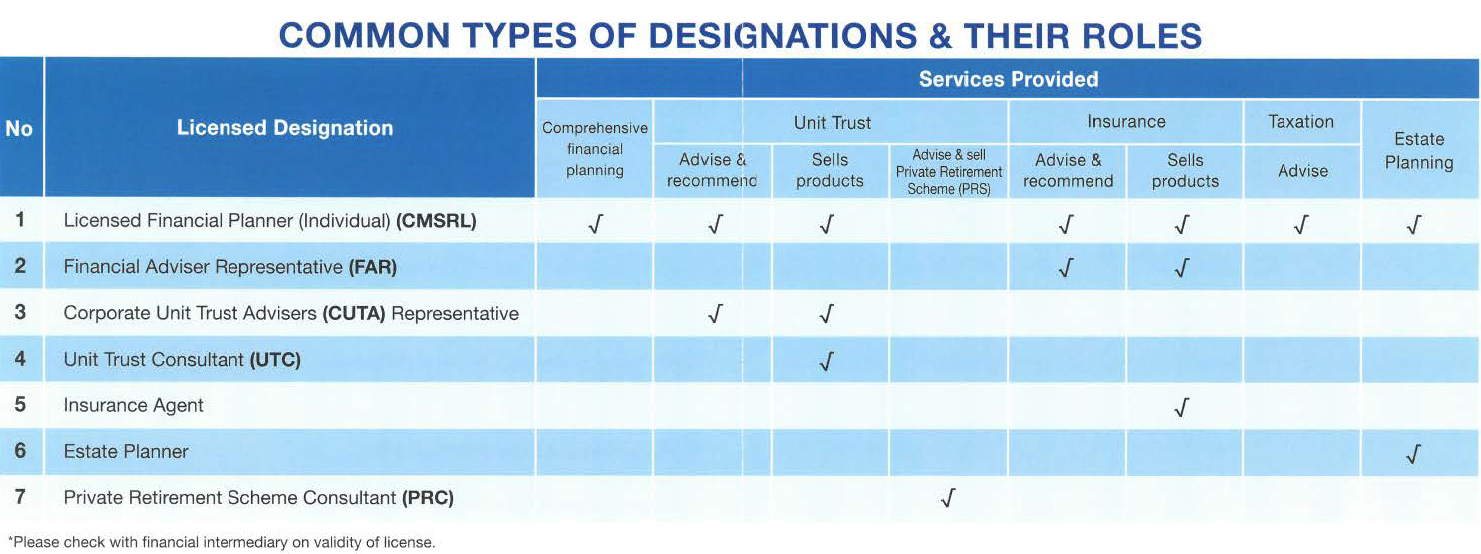

Financial intermediaries to reach out to

Q&A Session with Ms Kimberly

Q1: How would you know if you can/cannot afford a home? Should students/fresh grads look to rent or buy a home?

Answer: There are many factors to consider before buying/ renting a house.

- Living expenses.

- It’s a viable option if one spends less than 50% of their pay in living expenses.

- Cost/ Rental of the property.

- One has to allocate their money for the down payment which can be a burden.

- Cost efficiency.

- Transportation

- Location

- Convenience

Q2: Is it essential to have a credit card? i.e. to build a good credit rating? Does it affect the interest rate offered by banks when we want to take out a loan? i.e. house loan later on.

- Good to have credit card with a good self-control / cashflow management

- To Improve credit score

- Can you pay off the balance every month?

Q3: How should we balance our income with the loans we have (e.g. car loans and housing loans) so that we don’t overspend and still be able to have at least some form of savings?

- Refer to previous example

- Set aside savings (at least 20%)

- Loans are expenses so try not to incur as much as possible.

PERSONAL FINANCE IS A LIFELONG JOURNEY,

START EARLY AND MAKE GOOD CHOICES!

Who’s FLY Malaysia?

FLY Malaysia is a team of students all with a common goal in mind, to improve the standard of financial literacy among youths. The organization was founded in July 2015 by 2 students from the London School of Economics and Political Science (LSE), Nur Izzat Aiman bin Nur Aziz (BSc Accounting and Finance) and Adam Tiam Wen Yong (BSc Actuarial Science).

Written by: Alex and Nicholas

Edited by: Pei Zoe